A Special Report · Small Business Credit

– What Borrowers Need to Know in 2026.

If you took out an SBA COVID Economic Injury Disaster Loan — particularly one over $200,000 where you signed a personal guaranty — there is a reasonable chance you are now receiving collection notices, wage garnishment notices, Treasury Offset notifications, or letters about a 30% surcharge being added to your loan balance. This piece explains what happened, why it happened, what changed in March 2026, and what your options are.

I have been watching this problem develop since early 2023, before most lawyers and most borrowers were paying attention. What follows is a plain-language summary of how we got here, what is happening now, and what to think about if you are caught in the middle of it.

– I / ORIGN

How I came to this issue — 2023.

In early 2023, I was working with restaurant, hospitality, and small-business clients on COVID-era issues — lease restructurings, debt workouts, succession questions — and I started noticing a pattern. Many of my clients had taken out SBA COVID EIDLs of $300,000 to $2,000,000 (the program cap), secured by their business assets and backed by personal guaranties. Almost without exception, the businesses had limited remaining lease terms, finite enterprise values, and no realistic path to paying back six- or seven-figure EIDLs over a 30-year amortization once the deferment period ended.

I reached out to my contacts at the SBA and in adjacent federal-government roles. They shared with me what was, at the time, a quietly circulating Congressional Research Service report —

SBA COVID-19 EIDL Financial Relief: Policy Options and Considerations

(R47509). The CRS report confirmed in detail what I was already thinking: this was a structural problem, not an isolated one, and Congress was already discussing how to address it.

I have been monitoring the issue ever since, including through the November 2024 update of that same CRS report, the August 2025SBA Office of Inspector General report on delinquent COVID EIDL collections, and through ongoing conversations with SBA personnel, trade-association leadership, and other operators. The shape of the problem has been visible for years. What is new in 2026 is that the collection apparatus is now active.

– II / DIAGNOSIS

The core problem, in plain terms.

The SBA’s Economic Injury Disaster Loan program is decades old. It was originally designed for hurricanes, earthquakes, floods, and similar discrete natural disasters affecting specific geographic areas. Pre-COVID EIDLs were typically modest in size, made to a relatively small population of affected borrowers, and underwritten with attention to creditworthiness and collateral.

The COVID-19 pandemic broke that model in three ways at once — each unprecedented on its own, and unprecedented in combination.

– II / DIAGNOSIS, CONTINUED

Three breakdowns, at once.

— 01 / UNPRECEDENTED SCALE

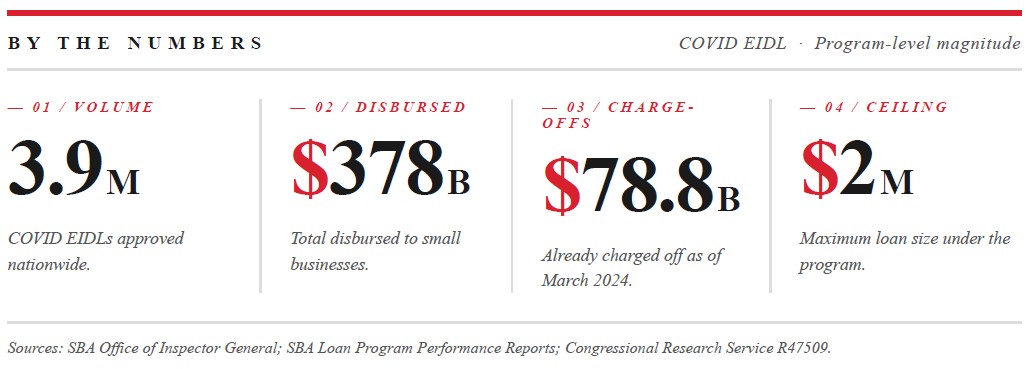

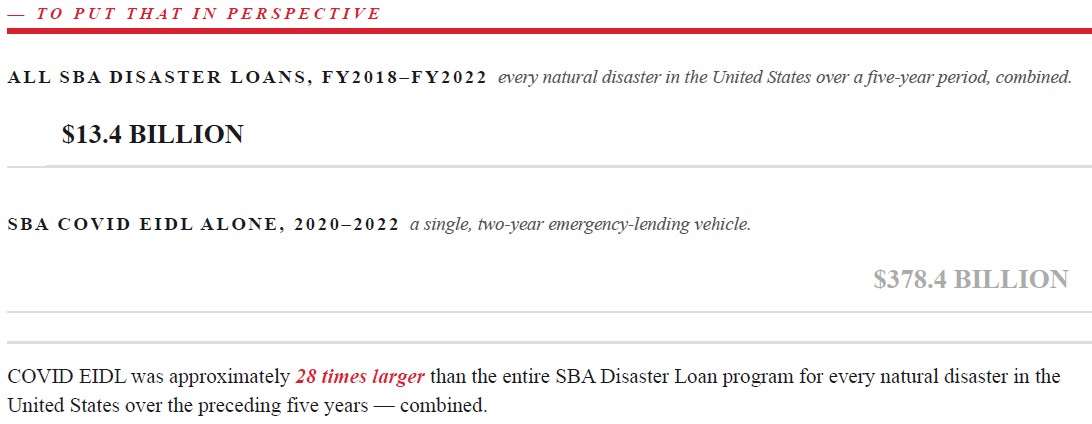

3.9 million loans. $378 billion in principal.

The SBA approved over 3.9 million COVID EIDLs, totaling more than $378 billion in original principal — orders of magnitude larger than any prior EIDL deployment in the program’s history.

— 02 / UNPRECEDENTED USE CASE

A discrete-shock instrument used through a multi-year national emergency.

EIDLs were not designed for a multi-year national pandemic. They were designed for businesses recovering from a discrete shock. COVID kept extending. Many borrowers used EIDL proceeds for ongoing operating expenses over multiple years, not as bridge funding through a recovery period. The loan structure (30-year amortization, modest fixed interest rate) was not calibrated for a borrower whose underlying business was already operating on the margin before the loan was disbursed.

— 03 / EFFECTIVELY ZERO UNDERWRITING

Grant-program risk management on a loan-program book.

Under emergency authority granted by Congress, the SBA waived its normal “credit available elsewhere” requirement, approved many loans based solely on credit score, and waived personal-guaranty requirements for loans up to $200,000. Loans of $25,000 or less required no collateral at all. The result: a multi-hundred-billion-dollar federal lending program deployed at speed with risk-management practices closer to those of a grant program thana loan program.

None of this is contested. The CRS report acknowledges it directly. The SBA Office of Inspector General has documented it repeatedly. The Government Accountability Office has flagged it. Congress is fully aware. The question has never been whether there would be a default wave. The question has been when the SBA would activate the collection apparatus that produces it.

– III / THE ACTIVATION

What changed at the end of March 2026.

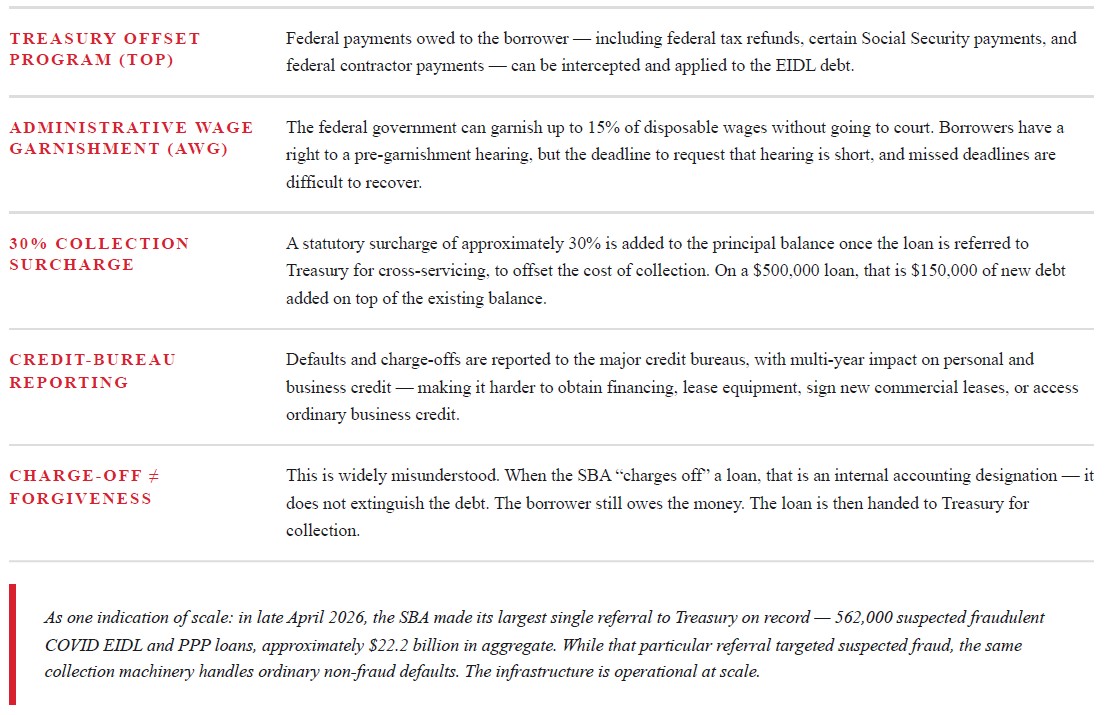

Throughout the deferment period (which the SBA extended multiple times — most recently to 30 months from the date of the note) and through the years immediately after, the SBA exercised significant restraint in collection. In particular, the SBA had been exempting most COVID EIDL borrowers from referral to the U.S. Department of the Treasury for cross-servicing collection — meaning that even where a borrower was in de‐fault, the more aggressive federal collection tools were not being deployed.

That cross-servicing exemption expired on March 31, 2026. Since that date, the SBA has been actively referring delinquent COVID EIDL borrowers to Treasury for cross-servicing. What that means in practice:

If you are receiving collection notices from a Treasury contractor, AWG hearing notices, or seeing tax refund interceptions or surcharge assessments, this is the reason. It is not a glitch in the SBA’s system. It is the activation of a collection regime that had been deferred for several years and that, since March 31, 2026, is now operating at full capacity.

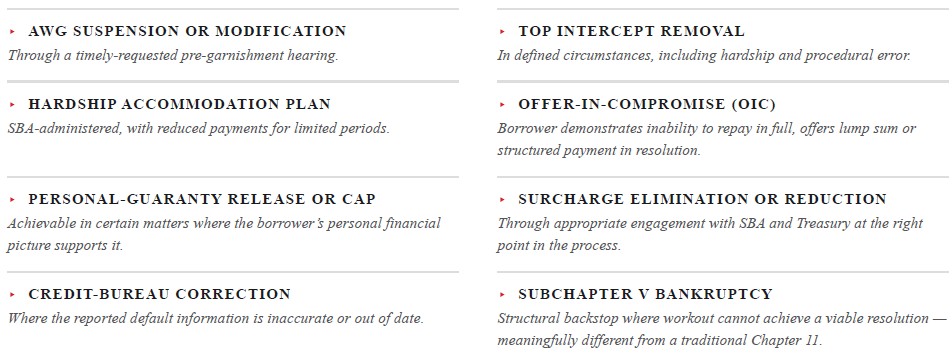

– IV / OPTIONS

What this means for you.

The honest answer is that the borrower is not without options. The SBA and Treasury both maintain procedures — some statutory, some administrative — through which a borrower’s situation can be addressed. Properly engaged, the following outcomes are achievable in many matters:

Each of these requires substantive engagement with the SBA and, in many cases, with Treasury’s Bureau of the Fiscal Service. Each has procedural deadlines that, once missed, are difficult or impossible to recover. Most cannot be resolved by phone with a Treasury collection contractor at a call center.

– V / TIMING

Why timing matters.

The political and legislative landscape around COVID EIDL is actively moving. The CRS report itself outlines four categories of policy options under congressional consideration — reduced interest rates, deferments without accrued interest, grant assistance, and loan forgiveness. Various legislative proposals to provide structural relief have been introduced. Whether any of them advance, and on what terms, remains uncertain.

What is not uncertain is that the borrower’s posture in any future structural relief framework — current versus delinquent, working with counsel versus not, in active negotiation versus in passive default, with a personal guaranty intact versus already capped or released — will materially affect the borrower’s eligibility and outcome under whatever framework eventually arrives.

– VI / AUTHOR

A note on me, and the firm.

I am a partner at Davidoff Hutcher & Citron LLP in New York City, where I lead the firm’s Hospitality & Restaurant Law Group. I have been working on EIDL and SBA-related matters with restaurant, hospitality, and small-business clients for several years, and I have been studying this default wave specifically since 2023. The firm has cross-departmental capability that is unusual for a regional firm — corporate workout, bankruptcy and Subchapter V representation, and long-standing government relations practices at the city, state, and federal levels (including with the SBA) — which we deploy in coordinated fashion on EIDL matters.

If you are facing an EIDL collection notice, an AWG hearing, a Treasury Offset, a 30% surcharge assessment, or any of the related is‐sues described above, I welcome the conversation. The earlier in the process you engage, the more options remain on the table.

—————————————————

About the Author

Andreas Koutsoudakis is a Partner and Co-Chair of the Hospitality & Restaurant Law Group at Davidoff Hutcher & Citron LLP. His practice focuses on the restaurant and hospitality industry, backed by the firm’s more than 50 years of experience representing New York businesses. He can be reached at aak@dhclegal.com.

This article is for informational purposes only and does not constitute legal advice. Every situation is different, and you should consult with qualified counsel to evaluate your specific circumstances.