Using a Section 363 Sale to Resolve an SBA EIDL Loan—and Release the Personal Guarantor

Here is the situation I see again and again. A business owner took out an SBA COVID EIDL loan to survive the pandemic. The loan was large enough to require a personal guarantee. The business has since struggled—maybe it’s closing, maybe it’s being sold—and the owner is terrified of one thing above all: that even after the business is gone, the SBA will come after them personally for the rest of their life.

That fear is well founded. Simply closing the business does not make a personal guarantee disappear. Neither, by itself, does the company’s bankruptcy. But there is a path—one I’ve used—that can deliver a genuinely clean exit: a Chapter 11 (often Subchapter V) case that uses a Section 363 sale to liquidate the assets, applies the proceeds to the SBA loan, and pairs that with a negotiated settlement that releases the personal guarantor. When it works, the SBA closes its file on both the company and the owner.

Let me walk through how the pieces fit together—and, just as importantly, where the real work lies.

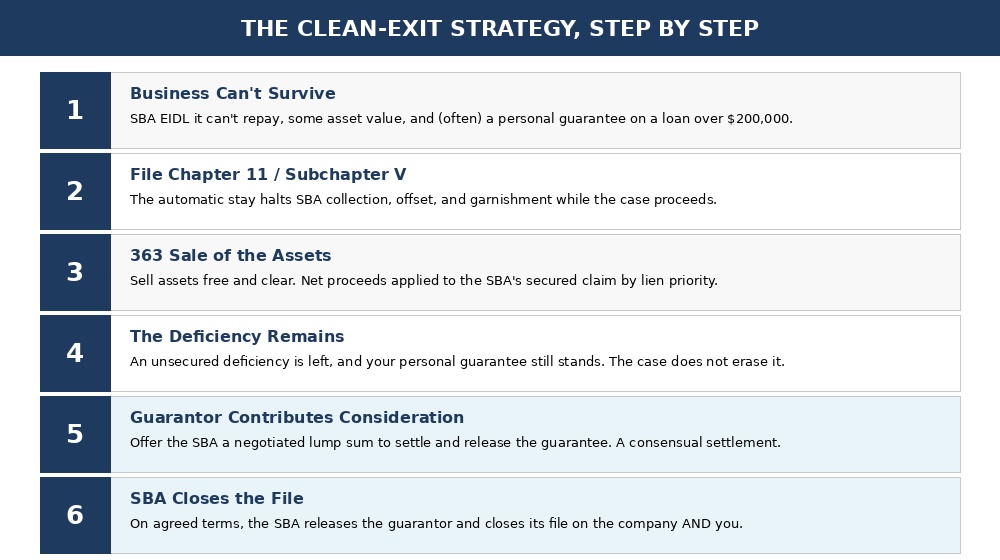

The Strategy in One Picture

At a high level, the plan moves from a failing business with a personally guaranteed loan to a complete, file-closed resolution:

FIGURE 1: The Clean-Exit Strategy

Step One: Liquidate the Assets Through a 363 Sale

Once the entity files, a Section 363 sale lets it sell its assets—equipment, fixtures, inventory, brand, leasehold—free and clear of liens, under court supervision. The net proceeds are distributed to creditors according to their priority.

For most EIDL borrowers, the SBA holds a blanket UCC lien on the business assets (required for loans of $25,000 or more). That makes the SBA a secured creditor as to those assets, so the sale proceeds are applied to its loan first, up to the value of its collateral. Whatever the assets fetch reduces the SBA’s claim dollar-for-dollar.

The 363 sale does the heavy lifting on the company’s side of the ledger. But it almost never pays the SBA in full—and that’s where the second, separate problem begins.

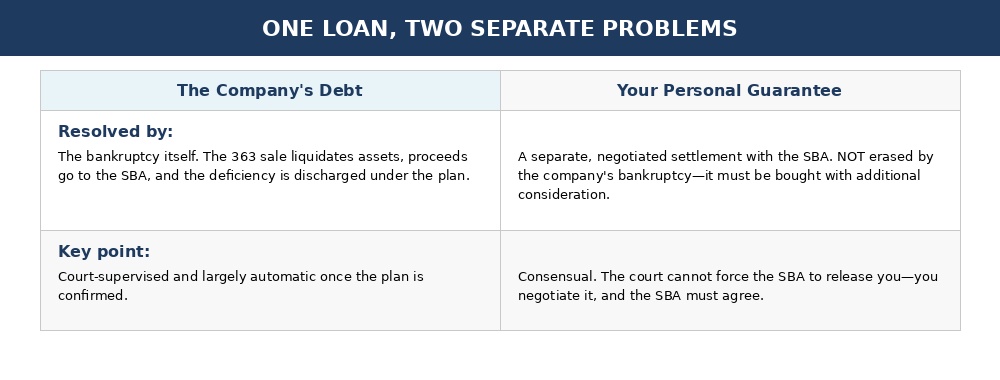

Step Two: Understand What the Bankruptcy Does NOT Solve

After the assets are sold, there is usually a deficiency—the unpaid balance above what the collateral covered. On the company’s side, that deficiency becomes an unsecured claim that is discharged or treated under the plan. The company walks away clean.

You, the guarantor, do not—at least not automatically. This is the single most misunderstood point in the entire process. The discharge of the company’s debt does not discharge your personal guarantee. The SBA can still pursue you individually for the deficiency, including through Treasury offset and wage garnishment. The bankruptcy protected the business; it did not protect you.

FIGURE 2: One Loan, Two Separate Problems

Step Three: Buy Your Release With Additional Consideration

Because your guarantee survives, the release has to be negotiated—and paid for. This is the part that takes skill, and it’s the part that delivers the clean exit.

The mechanics: alongside the 363 sale, the guarantor offers the SBA a separate, additional payment—a lump sum—in exchange for a release of personal liability. This is, in substance, an offer in compromise of the guarantee. The SBA evaluates it the way it evaluates any settlement: what can it realistically collect from this guarantor, over what time, at what cost—versus a certain payment now? When the math favors the certain payment, the SBA agrees to release the guarantor and close the file.

Two things are essential to understand here. First, this release is consensual. A bankruptcy court generally cannot force the SBA to release a non-debtor guarantor; the U.S. Supreme Court reinforced that limit in 2024. So the release isn’t something the court hands you—it’s something you negotiate, and the SBA must agree. Second, it requires additional consideration—new value beyond what the estate is already paying. The contribution can come from your own funds, from family, or as part of a buyer’s deal, but it has to be real and separate.

If there is more than one guarantor, plan for each of them. Settling and releasing one guarantor does not release the others—the SBA can, and typically will, reserve its rights against any guarantor who hasn’t separately bargained for a release. Everyone who signed needs to be part of the deal to walk away clean.

Why the SBA Says Yes

Settling makes economic sense for the SBA, not just for you. Chasing an individual guarantor is slow and expensive, recoveries are uncertain, and a guarantor with limited assets may yield little after years of collection effort. A defined lump sum today, on top of the sale proceeds, is often the best realistic outcome the agency can expect. Framing the offer around that reality—what the SBA nets by settling versus what it nets by pursuing you—is the heart of the negotiation.

And this is established practice, not theory. The SBA has long held statutory authority to compromise a debt—including a guarantor’s liability—for less than the full balance (15 U.S.C. § 634(b)), and it uses it. In one SBA administrative decision, the agency released an individual guarantor on a roughly $425,000 loan in exchange for a $70,000 lump-sum payment, applied the business’s liquidation proceeds and that payment against the balance, and reserved its rights against the remaining guarantors (Luverne Dwyer, SBA No. 311). The same compromise authority applies to today’s COVID EIDL guarantees.

Timing helps too. The window to resolve a loan directly with the SBA narrows once it is referred to Treasury for collection, so moving while the matter is still within the SBA’s control generally preserves more flexibility.

The End State: A Closed File

When the strategy comes together, the result is what every guarantor in this position actually wants: the assets are sold, the proceeds go to the SBA, the company’s debt is resolved through the plan, and the guarantor’s additional contribution settles the personal exposure. The SBA closes its file on the borrower and the guarantor. No lingering deficiency. No offset. No garnishment. A real ending.

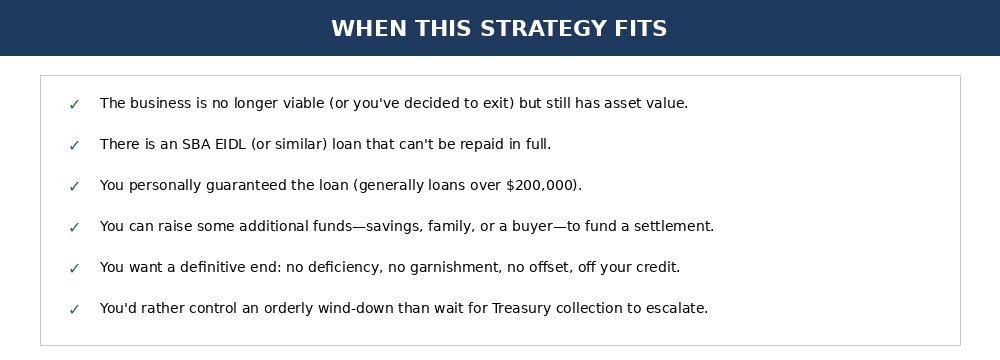

When This Strategy Fits

This is not the answer for every EIDL borrower—someone who is current and can keep paying shouldn’t be filing bankruptcy. But for an owner whose business has run its course and who carries a personally guaranteed SBA loan, it can be the cleanest available path:

FIGURE 3: When This Strategy Fits

Conclusion

A 363 sale and a guarantor settlement are two different tools solving two different problems—the company’s debt and your personal exposure. Used together, and in the right order, they can turn a frightening, open-ended SBA liability into a finished chapter.

The key is to plan both halves from the start, because the guarantor release isn’t automatic—it’s negotiated, it’s paid for, and it depends on the SBA agreeing. If you’re facing a personally guaranteed EIDL on a business that can’t carry it, the time to build the strategy is before the collection machinery escalates. Let’s talk.

—————————————————

About the Author

Andreas Koutsoudakis is a Partner and Co-Chair of the Hospitality & Restaurant Law Group at Davidoff Hutcher & Citron LLP. His practice focuses on the restaurant and hospitality industry, backed by the firm’s more than 50 years of experience representing New York businesses. He can be reached at aak@dhclegal.com.

This article is for informational purposes only and does not constitute legal advice. Every situation is different, and you should consult with qualified counsel to evaluate your specific circumstances.