When the Investor You Needed Becomes the Partner You Can’t Escape

Founding Chef vs. Money Partner — The Chef’s Perspective

- This white paper is based on a composite of real cases handled by the DHC Hospitality & Restaurant Law Group. Names, locations, cuisines, and identifying details have been changed to protect client confidentiality. The legal principles discussed are illustrative and should not be relied upon as legal advice for any specific situation.

Almost every restaurant starts the same way: someone with talent meets someone with money, and for a while, that is enough. The chef brings the concept and the hands. The investor brings the check. They shake on it, they open the doors, and the food is good enough that nobody looks too hard at the paperwork. I have spent a good part of my career on what happens after that — when the handshake meets the operating agreement, and the two of them don’t agree.

This is the story of a chef who did everything right in the kitchen and almost lost half of it anyway. It is also a story about a five-minute email that never got sent.

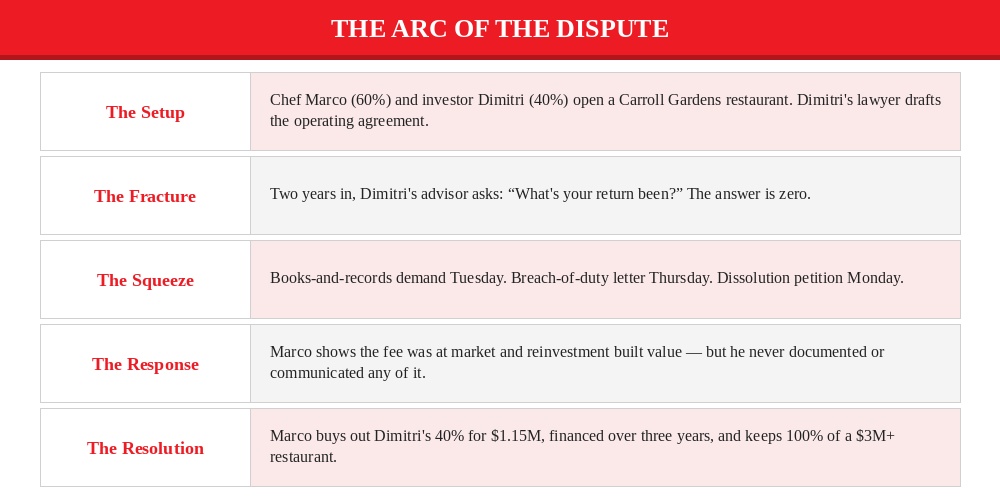

The Setup

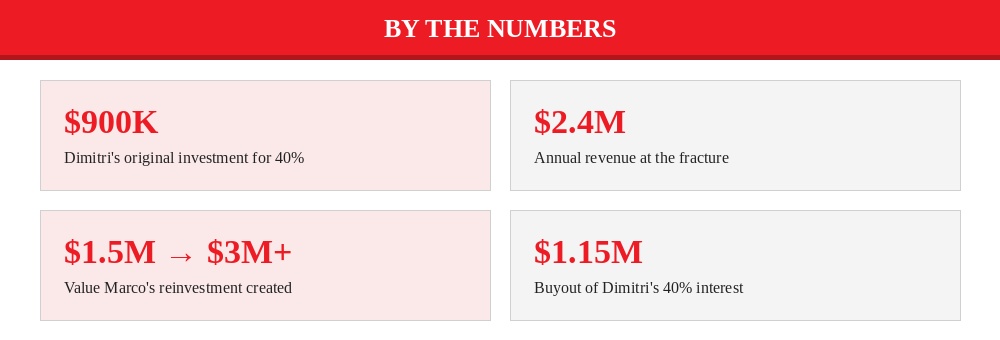

Marco had been cooking since he was fourteen — first in his father’s diner in Astoria, then through culinary school, then through a decade of eighty-hour weeks in other people’s kitchens. By the time he was thirty-five, he had a following, a concept, and a location picked out on a tree-lined block in Carroll Gardens. What he didn’t have was nine hundred thousand dollars.

That is where Dimitri came in. A real estate investor with a taste for Greek food and a portfolio of rental properties, Dimitri saw an opportunity, and he wrote the check. They formed an LLC. Marco got sixty percent, Dimitri got forty. The operating agreement — drafted by Dimitri’s attorney, a detail that matters more than Marco understood at the time — made Marco the managing member with authority over “day-to-day operations,” and made distributions payable “at the discretion of the managing member.” Both men signed it. Neither of them read it the way a lawyer would have.

The Fracture

For two years, the restaurant thrived. Marco worked the line six nights a week. Dimitri stopped by for dinner on Saturdays, complimented the lamb, and asked if things were “going well.” Marco said yes, and the numbers backed him up — the restaurant was doing $2.4 million in annual revenue at an eleven percent net margin. By any operator’s standard, that is a hit.

The fracture started with one question from a financial advisor Dimitri had hired to look at his portfolio: “You invested nine hundred thousand dollars two years ago. What’s your return been?” The honest answer was zero. Marco had been paying himself a $240,000 management fee — reasonable for a managing chef at a restaurant that size — and pouring everything else back into the business: new equipment, a kitchen renovation, a private dining room buildout. No distributions had ever been declared. From where Marco stood, he was building something. From where Dimitri now sat, he was being cut out of his own investment.

Both of them were, in a sense, right. That is what makes these cases hard. Nobody had stolen anything. The disagreement was about what the money was for — and the operating agreement, which should have answered that question, had instead handed Marco “discretion” and left it there.

The Squeeze

Dimitri’s attorney sent a books-and-records demand on a Tuesday. A books-and-records demand is exactly what it sounds like — a formal request, backed by statute, for the financial records a member is entitled to inspect. It is almost always the first move, because it is the move that builds the file for everything that follows.

By Thursday, Marco had a letter accusing him of breach of fiduciary duty, self-dealing, and oppression. By the following Monday, Dimitri had filed a petition for judicial dissolution — asking a court to wind the company down and, in effect, force a sale. Marco was blindsided. He had been so focused on running the restaurant, the thing he was actually good at, that he never noticed the legal machinery assembling around him.

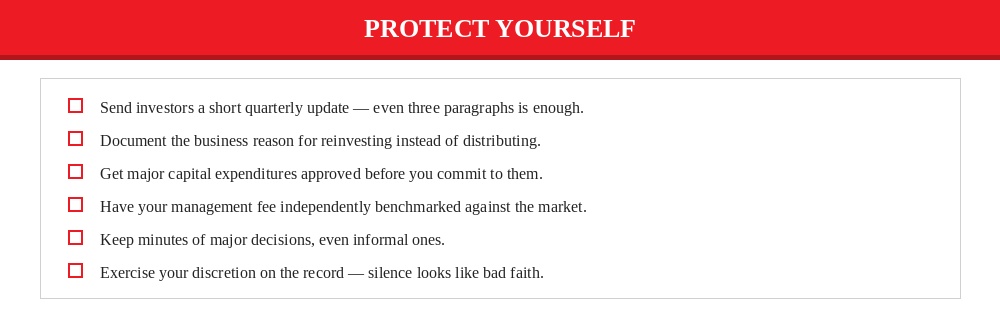

And here is the cruel part. Every decision Marco had made in good faith now looked like a squeeze-out on paper. He hadn’t kept minutes. He hadn’t written down the business reasons for reinvesting instead of distributing. He had never had the management fee independently benchmarked. He hadn’t told Dimitri what the kitchen renovation would cost before committing to it. The good faith was real. The paper trail that would have proven it did not exist.

The Response

Marco’s attorney went to work reframing the story, because the facts, properly assembled, were on Marco’s side. The management fee was at market — industry surveys put managing chefs at comparable restaurants between $200,000 and $280,000. The reinvestment decisions were sound business judgments that had taken the restaurant from a $1.5 million enterprise at opening to one worth more than $3 million by the time Dimitri filed. The absence of distributions reflected a growth phase, not a freeze-out: the agreement gave Marco discretion, and he had used it to build equity rather than write checks.

But there was no getting around Marco’s one real mistake. He had communicated none of this. No quarterly reports. No investor updates. No record of why he was making the calls he was making. Discretion exercised in silence looks identical, on paper, to discretion exercised in bad faith. A court can’t see the difference, and an angry partner won’t.

The Resolution

The case settled at mediation. Marco bought out Dimitri’s forty percent for $1.15 million — a price that reflected the restaurant’s increased value, which Marco’s own reinvestment had created, discounted for the risk and expense of fighting it out in court. Marco financed the buyout over three years, secured by the restaurant’s assets. Dimitri walked away with a real return on his investment. Marco walked away owning one hundred percent of a restaurant worth more than three million dollars.

The Lesson

Marco’s story is the founding chef’s cautionary tale, and the lesson is not the one most chefs expect. Doing the right thing for the business is not enough if you don’t document it, communicate it, and get approval for it. The operating agreement asked Marco to exercise discretion over distributions. He did — reasonably, even wisely. But discretion exercised quietly, with no record and no explanation, is the easiest thing in the world for a disappointed investor’s lawyer to recast as oppression.

If Marco had sent Dimitri a single quarterly email — three paragraphs, five minutes — explaining what the reinvestment was funding and when distributions would resume, this entire dispute very likely never happens. Not because the email is legally magic, but because it turns a silent decision into a documented, communicated, defensible one.

The lesson for every chef-owner is short enough to tape to the walk-in: your food doesn’t speak for itself in a courtroom. Your documentation does.

—————————————————

If you recognize your situation in this story, you’re not alone — and you have options.

The DHC Hospitality & Restaurant Law Group represents restaurant and hospitality owners in business divorce, partnership disputes, and ownership transitions throughout New York, backed by the firm’s more than 50 years of experience representing New York businesses.

Contact us for a confidential consultation:

Andreas Koutsoudakis, Esq. | Partner & Co-Chair

(212) 557-7200 | aak@dhclegal.com

This article is for informational purposes only and does not constitute legal advice. Every situation is different, and you should consult with qualified counsel to evaluate your specific circumstances.